March 11th, 2026

“You Can’t Take the Same Action As Everyone Else And Expect To Outperform” — Howard Marks

1. US Companies Added 63,000 Jobs in February, ADP Data Show — Private-sector payrolls increased 63,000 in February after a downward revision to the prior month, according to ADP Research data out Wednesday. The median estimate in a Bloomberg survey of economists called for a 50,000 advance. Federal Reserve officials generally see the job market as stabilizing, which should allow them to keep interest rates unchanged in the near future so that they can focus on stubborn inflation. Policymakers this week have said it’s too soon to assess how the war in Iran will impact the US economy. The advance in hiring was led by education and health services, which has been responsible for the majority of job creation in the last year. Construction and information also added to payrolls. The strongest hiring was seen in the South as well as at businesses with fewer than 20 employees.

2. BlackRock Slashed Another Private Loan Value From 100 to Zero — The roughly $25 million loan to Infinite Commerce Holdings, a so-called Amazon aggregator that buys up online sellers of products from spa treatments to light bulbs, is now worthless, BlackRock TCP Capital Corp. reported in fourth-quarter filings released last week. The fund had marked the junior debt at 100 cents on the dollar in the third quarter. The moves add to mounting concerns over defaults and underwriting standards in the $1.8 trillion private credit market. The industry’s huge bet on software companies threatened by AI has led to unprecedented redemption demands by jittery investors. Blackstone Inc. announced on Monday it would allow investors to redeem a record 7.9% of shares from its flagship private credit fund.

3. China Signals New Era of Slower Economic Growth — China signaled that the world’s second-largest economy is entering an era of slower expansion, setting a target for gross domestic product growth of between 4.5% and 5% this year.

It is the lowest target set since at least the 1990s and follows three years in which officials called for growth of “around 5%.” If China’s economy were to expand at a pace below 5% this year, it would be the slowest growth reported by the country in more than three decades, other than during the Covid-19 pandemic years.

4. U.S. Loses 92,000 Jobs in Widespread and Unexpected Downturn — Nonfarm payrolls fell 92,000 last month, one of the largest declines since the pandemic, after a strong start to the year. While some of the downside was expected in advance, like a temporary dent from striking healthcare workers and a potential hit from bad weather, a wide array of industries cut jobs in the month. Job report from the Bureau of Labor Statistics suggests companies may be starting to follow through on a series of previously announced layoffs. And a recent trend in productivity gains illustrates how spending on artificial intelligence has allowed some firms to get by with leaner staffing. The figures could refocus the Fed’s attention on the jobs market as it assesses how long to hold interest rates steady. Policymakers have been more attuned to inflation lately — even before the US-Israeli war on Iran sparked concerns among investors about price pressures.

The week ahead — Economic data from Econoday.com:

Posted in Weekly Summary | No Comments »

March 4th, 2026

We are away for the Week of March 1st 2026 for some needed R&R — Have a good week!!

The week ahead — Economic data from Econoday.com:

Posted in Weekly Summary | No Comments »

February 27th, 2026

“Absorb what is useful, discard what is not, add what is uniquely your own”. — B. Lee

1. Fed Minutes Show Several Officials Nod to Rate-Hike Scenario — Federal Reserve officials signaled renewed worries over inflation with “several” policymakers suggesting the central bank may need to raise interest rates if inflation stays above their goal. Minutes of the Federal Open Market Committee’s Jan. 27-28 meeting released Wednesday also revealed that a “vast majority of participants judged that downside risks to employment had moderated in recent months while the risk of more persistent inflation remained.” Several officials saw the likelihood for more rate cuts if inflation declined as they expected, though most said inflation progress could be slower than generally forecast.

2. US Notches One of Its Biggest Annual Trade Gaps Since 1960 — The goods and services trade gap expanded from the prior month to $70.3 billion, Commerce Department data showed . The shortfall culminated in a full-year deficit of $901.5 billion, still one of the largest in data back to 1960. The December deficit — which was wider than all but one estimate in a Bloomberg survey of economists — reflected a 3.6% increase in the value of imports, including gains in computer accessories and motor vehicles. Exports of goods and services declined 1.7%, largely reflecting fewer outbound shipments of gold. After the report, several economists estimated trade would provide a smaller boost, or even a drag on fourth-quarter gross domestic product, which is due Friday. The latest GDPNow forecast from the Federal Reserve Bank of Atlanta reflected as much, predicting net exports will barely add to fourth-quarter growth, now estimated at 3%.

3. US GDP Grows 1.4%, Missing Forecasts on Shutdown, Trade — Inflation-adjusted gross domestic product increased an annualized 1.4% in the fourth quarter after rising 4.4% in the prior period, according to the government’s initial estimate. Overall, the economy expanded 2.2% last year, data from the Bureau of Economic Analysis showed.

The weak quarterly result — which was below all forecasts in a Bloomberg survey of economists — came as the US government was shut down for almost half of the three-month period. The BEA said the reduction in federal services during the shutdown subtracted about 1 percentage point from GDP, though the full impact couldn’t be estimated.Despite the year-end slowdown, the data still cap a solid year for the US economy, which shrank in the first quarter amid a monumental pre-tariff surge in imports, only to bounce back later in the year. The turnaround came after Trump backed off of his most punitive levies and the Federal Reserve lowered interest rates, helping drive the stock market to record highs and enabling wealthier Americans to keep spending.

The week ahead — Economic data from Econoday.com:

Posted in Weekly Summary | No Comments »

February 18th, 2026

“Do More of What Works & Less of What Does Not”

1. US Consumer Delinquencies Jump to Highest in Almost a Decade — Delinquency rates on loans ranging from mortgages to credit cards rose to 4.8% of all outstanding US household debt in the fourth quarter, the highest level since 2017, driven by higher defaults among low-income and young borrowers. While the overall share of loans in some stage of default is near pre-pandemic averages, the rise in delinquencies among the lowest earners adds to evidence of an increasingly bifurcated economy, data from the Federal Reserve Bank of New York’s Quarterly Report on Household Debt and Credit released showed. The rise in defaults was driven by delinquencies in mortgage payments, and New York Fed researchers found that they were particularly high in lower income zip codes. Student-loan delinquencies, which have surged following a pause in payment requirements during the pandemic, also contributed to the rise in defaults, the researchers said.

2. December Retail Sales Fell Short. Worries About the Economy Curbed Holiday Spending — Retail sales were virtually unchanged in December from November, according to data released Tuesday by the Census Bureau. Economists polled by FactSet expected a 0.4% increase. While that would have marked a slight deceleration from November’s 0.6% rise, it would have indicated that spending was healthy throughout the holiday season. The biggest drops came among retailers of miscellaneous goods and furniture stores, both with declines of 0.9% in December from November. Sales fell 0.7% and 0.4% at clothing stores and electronic stores, respectively. Car dealers, general merchandise stores, health and personal care stores, and restaurants also saw declines from November.

3. Fed’s Path to More Rate Cuts Challenged by Jobs Surprise — Worries about rising unemployment that prompted three rate cuts at the end of 2025, before a pause in January, were likely eased by numbers out Wednesday showing 130,000 jobs were added last month, and unemployment fell to 4.3%. Fed officials at last month’s policy meeting had already cited signs of stabilization as a reason to hold rates steady. Wednesday’s report from the Bureau of Labor Statistics prompted traders to pare the probability of a rate cut at the June meeting — previously eyed as the most likely timing of the next reduction — to under 50%. Economists cautioned that the upbeat January numbers could yet be revised lower, and that hiring continues to be dominated by a handful of sectors, primarily health care. Revisions to last year’s data showed job gains averaged just 15,000 a month, down from the initially reported 49,000 pace.

4. Home Sales in January Posted Biggest Monthly Decline in Nearly Four Years — Home sales fell 8.4% in January, the biggest monthly decline since February 2022, after snowstorms and low consumer confidence slowed a housing market that was showing signs of recovery. Sales of existing homes fell from the prior month to a seasonally adjusted annual rate of 3.91 million, the National Association of Realtors said. Home prices continued to rise, because the national supply of homes for sale remains below normal historical levels. The national median existing-home price in January rose to $396,800, a 0.9% increase from a year earlier, NAR said. Mortgage rates stand around 6.1%, down from about 6.9% a year ago. That is helping make purchases a little more affordable.

5. Consumer prices rose 2.4% annually in January — The consumer price index for January accelerated 2.4% from the same time a year ago, down 0.3 percentage point from the prior month, the Bureau of Labor Statistics reported Friday. That pulled the inflation rate down to where it was the month after President Donald Trump in April 2025 announced aggressive tariffs on U.S. imports. Excluding food and energy, the core CPI was up 2.5%, the lowest level since April 2021. Economists surveyed by Dow Jones had been looking for an annual rate of 2.5% for both readings. Elsewhere, food prices increased 0.2% as five of the six major grocery group categories posted gains. Energy fell 1.5% while vehicle prices also were muted, with new vehicles up just 0.1% and used cars and trucks falling 1.8%. Airline fares jumped 6.5% while egg prices fell 7% and are now down 34% over the past year after a meteoric surge.

The week ahead — Economic data from Econoday.com:

Posted in Weekly Summary | No Comments »

February 10th, 2026

“Trade what’s happening… not what you think is gonna happen.“ — Doug Gregory

1. U.S. Enlists Mexico, EU and Japan in Its Minerals Race With China — The U.S. has agreed to work with Japan, Mexico and the European Union on the development of critical minerals used in industries such as defense, the Trump administration said on Wednesday.

The move builds on President Trump’s efforts to combat China’s dominance in the sector. Under the proposed agreements, the nations will work together to identify critical minerals necessary for certain industries and develop policies to encourage their mining and processing into products like rare earth magnets, U.S. officials said. Such minerals are used in components critical for the production of high-end military technologies and consumer products such as cars.

2. Bitcoin Drops Below $70,000 as ‘Forced Deleveraging’ Accelerates — Bitcoin tumbled well below $70,000 as the unwinding of leveraged bets and broader market turbulence deepened a selloff that’s hammered cryptocurrencies over the past three weeks. The downturn has also erased all of Bitcoin’s gains since the election of President Donald Trump, whose crypto-friendly stance had fueled the token’s meteoric rise last year. But the market started cracking this month as rising geopolitical tensions sent tremors across global financial markets and curbed risk taking. That sparked Bitcoin’s precipitous decline from mid-January and set off a self-reinforcing cycle of selling as funds liquidated assets to meet redemptions and unwind leveraged bets.

3. Job Openings Sink to a Post Pandemic Low — The number of job openings in December fell to the lowest level in eight years, excluding the COVID-19 pandemic era, underscoring the fragility of the U.S. labor market in the new year. U.S. job openings dropped by 386,000 in December to 6.5 million, the government said in a report delayed by federal shutdowns. That’s the lowest total since 2017, excluding the 2020-21 time frame. The exceedingly small gap between hires and separations illustrates just how weak the labor market has gotten since last spring. The economy is barely adding net new workers.

The week ahead — Economic data from Econoday.com:

Posted in Uncategorized, Weekly Summary | No Comments »

February 4th, 2026

“Do More of What Works and Less of What Doesn’t” — unknown

1. Fed Holds Rates Steady, Nods to Stabilization in Jobless Rate — Federal Reserve officials left interest rates unchanged and pointed to improvements in the US economy as they signaled a more cautious approach to potential future adjustments. The Federal Open Market Committee voted 10-2 Wednesday to hold the benchmark federal funds rate in a range of 3.5%-3.75%. Governors Christopher Waller and Stephen Miran dissented in favor of a quarter-point reduction. The upgraded assessment of the labor market is likely to hold expectations for a near-term rate cut at bay, despite escalating pressure from the Trump administration. Heading into the meeting, investors saw another cut as unlikely until at least June.

2. Meta Reports Record Sales, Massive Spending Hike on AI Buildout — The company said capital spending would reach up to $135 billion in 2026, about 20% higher than Wall Street expectations and nearly double last year’s investment level. Chief Executive Mark Zuckerberg plans to build new data centers around the globe, release new cutting edge AI models and further infuse the core advertising business with AI this year.

3. US Trade Gap Widens From Smallest Since 2009 as Imports Rise — The goods and services trade gap nearly doubled from the prior month to $56.8 billion, Commerce Department data showed Thursday. The 94.6% widening was the largest since 1992, while the shortfall for the month exceeded all projections in a Bloomberg survey of economists. That was the case again in November, with a surge in inbound shipments of pharmaceuticals and a slide in gold exports. Overall imports increased 5%, also boosted by capital goods, such as computers and semiconductors. The latest trade data will help economists firm up their estimates for fourth-quarter gross domestic product. After the figures, the Federal Reserve Bank of Atlanta’s GDPNow forecast net exports would add 0.65 percentage point to fourth-quarter growth, now estimated at 4.2%.

4. Trump Picks a Reinvented Warsh to Lead the Federal Reserve — Warsh, who served on the US central bank’s Board of Governors from 2006 to 2011 and has previously advised Trump on economic policy, would succeed Jerome Powell when his term at the helm ends in May. It marks a comeback for Warsh, 55, whom the president passed over for the top job in 2017 when he selected Powell. If confirmed by the Senate, the former Fed governor will take charge of US monetary policy at a time when many economists and investors see its traditional insulation from elected officials as being under threat from the White House. Warsh aligned himself with the president in 2025 by arguing publicly for lower interest rates, going against his longstanding reputation as an inflation hawk.

The week ahead — Economic data from Econoday.com:

Posted in Weekly Summary | No Comments »

January 28th, 2026

“If most traders would learn to sit on their hands 50 percent of the time, they would make a lot more money.” — Bill Lipschutz

1. US Pending-Home Sales Plunge by Most Since Start of Pandemic — An index of contract signings decreased 9.3% to 71.8 last month, according to data released Wednesday by the National Association of Realtors. The decline was regionally broad and well below the lowest estimate in a Bloomberg survey of economists. Housing activity typically slows in winter

months and picks up more in the spring selling season. While NAR adjusts the data for these patterns, the drop was still the largest for any December in data back to 2001.

2. US Economy Expanded at Revised 4.4% Pace in Third Quarter — Inflation-adjusted gross domestic product, which measures the value of goods and services produced in the US, increased at a revised 4.4% annualized rate, the fastest in two years, according to Bureau of Economic Analysis data out. The report showed one of the strongest back-to-back quarters for growth since 2021, when the economy was still recovering from the pandemic. Companies dialed back the tempo of goods imports after an early-year rush to beat President Donald Trump’s sweeping tariffs. Consumer and business spending have also held up well despite erratic trade policies.

3. PCE Inflation Meets Expectations. Fed Is Likely to Hold Rates Next Week — The core personal consumption expenditures price index, which excludes food and energy, rose 0.2% in November from the previous month and 2.8% from a year earlier, the Bureau of Economic Analysis reported Thursday. Those figures match FactSet estimates for a 0.2% monthly increase and a 2.8% annual gain. Headline PCE increased 0.2% on the month and 2.8% year over year, compared with expectations for a 0.2% monthly rise and a 2.8% annual increase. Because the data were delayed by the record-long government shutdown, the numbers reflect conditions from November, already several months old. While PCE is the Fed’s go-to inflation metric, the age of the report means officials are likely to place less weight on this reading than they would under normal circumstances.

The week ahead — Economic data from Econoday.com:

Posted in Weekly Summary | No Comments »

January 21st, 2026

“I’m not better than the next trader, just quicker at admitting my mistakes and moving on to the next opportunity.” — George Soros

1. US Core CPI Rises 0.2%, Bucking Estimates for Bigger Rebound — The core consumer price index, excluding the often volatile food and energy categories, increased 0.2% from November, according to Bureau of Labor Statistics data out Tuesday. On an annual basis, it advanced 2.6%, matching a four-year low. Economists said that data was artificially depressed by the record-long government shutdown because the BLS couldn’t collect prices in October and assumed no increases in key housing metrics. November data were also collected later than usual and could have been affected by holiday discounts. Several categories showed price declines, including appliances and used cars and trucks. Vehicle repair costs fell by the most on record. Core goods prices, which exclude food and energy, stagnated last month — also defying expectations for a rebound.

2. Germany Leads Military Mission in Greenland in Response to Trump — Germany will take the lead of European nations sending military personnel to Greenland after Denmark said its meeting with top US officials intent on controlling the world’s biggest island revealed that a “fundamental disagreement” remains. France will participate in the joint drills in Greenland this week, according to the defense ministry’s press office, which provided no details. In addition, Sweden is sending “several officers,” Norway two persons and the UK one officer. The reconnaissance group is visiting the island ahead of the planned “Arctic Endurance” training exercise, UK Defense Minister John Healey told reporters in Sweden. Denmark on Wednesday said the drill with North Atlantic Treaty Organization allies would become a permanent fixture.

3. Trump Threatens Insurrection Act as Minnesota Protests Grow — The 1807 law allows the president to use regular military troops on US soil for domestic law enforcement. It was last invoked during the 1992 riots in Los Angeles. Trump’s ultimatum could further fray tensions in Minneapolis, where on Wednesday a federal officer shot a man in the leg. The incident occurred one week after the fatal shooting of a local woman who was a US citizen by an ICE agent, which touched off the demonstrations.

4. Trump to Hit European Nations With 10% Tariffs as He Presses for Sale of Greenland — The president, in a social-media post on Saturday, said the 10% tariffs would go into effect on Feb. 1 and would apply to all goods sent to the U.S. from Denmark, Norway, Sweden, France, Germany, the United Kingdom, the Netherlands and Finland. The tariffs will increase to 25% on June 1 and remain in place until a deal is reached for what he called the “complete and total purchase” of Greenland, Trump said. The president has said it is necessary for the U.S. to take control of Greenland to counter China and Russia. In his social-media post, he said the U.S. is “immediately open to negotiation” with Denmark and the other European countries, casting the tariff threat as leverage to secure the Arctic territory. Greenland Prime Minister Jens-Frederik Nielsen said recently that his constituents don’t want the island to be owned or controlled by the U.S.

The week ahead — Economic data from Econoday.com:

Posted in Weekly Summary | No Comments »

January 13th, 2026

1. US Job Openings Decline to Lowest Level in More Than a Year — The number of available positions decreased to 7.15 million in November from a downwardly revised 7.45 million in the prior month, Bureau of Labor Statistics data showed Wednesday. The figure was below all estimates in a Bloomberg survey of economists. The pullback in openings reflected fewer opportunities in leisure and hospitality, health care and social assistance, as well as transportation and warehousing. The number of hires declined to the lowest since mid-2024, while layoffs also eased. The number of layoffs in November declined to a six-month low after climbing in the prior month to the highest level since 2023, the JOLTS report showed. At the same time, there was a pickup in the number of Americans who voluntarily left their jobs in industries including accommodation and food services, as well as construction

2. US Trade Gap Shrinks to Smallest Since 2009 on Imports Drop — The goods and services trade gap shrank 39% from the prior month to $29.4 billion, Commerce Department data showed Thursday. The deficit was smaller than all estimates in a Bloomberg survey of economists. The report was delayed for over a month because of the federal government shutdown. Imports decreased 3.2%, reflecting declines in inbound shipments of medication and nonmonetary gold. Imports of pharmaceutical preparations dropped to the lowest since July 2022. The value of all US goods and services exports rose 2.6% in October. The figures aren’t adjusted for inflation. Companies frontloaded imports of drugs in September, likely in anticipation of President Donald Trump announcing what would be a 100% tariff on pharmaceutical imports to start Oct. 1, which ended up being delayed. Many companies were able to avoid the duty by striking deals with the administration in exchange for promises to lower drug prices.

3. US Payrolls Rise a Below-Forecast 50,000, Unemployment Lower — Nonfarm payrolls increased 50,000 last month after downward revisions to the prior two months, according to Bureau of Labor Statistics data out Friday. The unemployment rate edged down to 4.4%, settling back after the record-long government shutdown. The gradual cooling in the US labor market prompted the Federal Reserve to cut interest rates three straight times to close out 2025. While it was one of the weakest years for hiring since 2009, employers have also largely refrained from layoffs. The December data also suggest the labor market remained fragile at the end of the year, and the outlook for hiring is guarded. Economists see another year of limited job opportunities and cooling pay gains, likely exacerbating voters’ affordability concerns going into this year’s midterm elections.

4. SSupreme Court Sets Wednesday for Next Opinions Amid Tariff Watch — The US Supreme Court said Wednesday will be its next opinion day after leaving the market in suspense Friday on the fate of President Donald Trump’s tariffs, his signature economic policy. Arguments on Nov. 5 suggested the court was skeptical that Trump had authority to impose the tariffs under a 1977 law that gives the president special powers during emergency situations. A ruling against Trump on tariffs would undercut his signature economy policy and deliver his biggest legal defeat since returning to the White House. At issue are Trump’s April 2 “Liberation Day” tariffs, which placed levies of 10-50% on most imports, along with duties imposed on Canada, Mexico and China in the name of addressing fentanyl trafficking.

The week ahead — Economic data from Econoday.com:

Posted in Weekly Summary | No Comments »

December 30th, 2025

Happy Holidays and Wishing Everyone a Healthy and Prosperous New Year

1. US Economy Grows at Fastest Pace in Years With 4.3% GDP Gain — Inflation-adjusted gross domestic product, which measures the value of goods and services produced in the US, increased at a 4.3% annualized pace, a Bureau of Economic Analysis report showed Tuesday. That was higher than all but one forecast in a Bloomberg survey and followed 3.8% growth in the prior period.

The BEA was originally due to publish an advance estimate of GDP on Oct. 30, but the report was canceled due to the government shutdown. The agency typically releases three estimates of quarterly growth — fine-tuning its projections as more data comes in — but it will only release two for the period leading up to the longest shutdown on record.

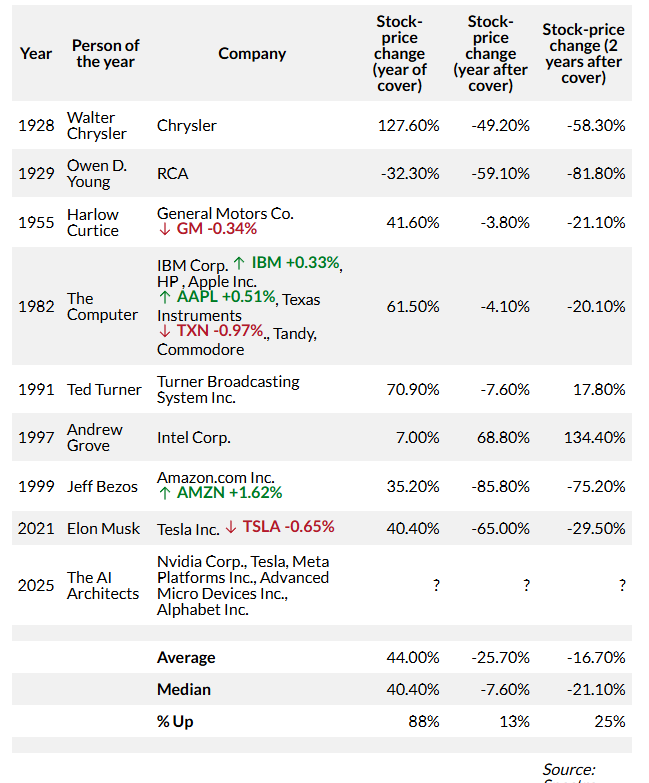

2. Time just jinxed the AI stock-market rally with its 2025 person of the year — Pioneered by analyst Paul Macrae Montgomery in his newsletter “Universal Economics,” the Time Magazine Cover Indicator — also known more generally as the Magazine Cover Indicator — posits that if a popular investment theme makes it to the cover of a general-interest publication like Time magazine, then the end is probably near. Time magazine announced its selection for person of the year. For 2025, it awarded the honor to a group of people, as it sometimes does: “The Architects of AI.” Brent Donnelly, president of Spectra Markets, crunched the numbers, and found that the person-of-the-year track record as a counterindicator is actually quite remarkable. Although the sample size is small, by Donnelly’s count — there have only been nine instances so far, including this year’s, in which the Time cover represented an investable person, company or category — it has been surprisingly effective. Investments, whether in companies or trends, tied to a person-of-the-year pick were higher one year later just 13% of the time, according to Donnelly. After two years, that figure rose to 25%. The only example that didn’t sell off during the following year was Intel Corp., whose co-founder and then-CEO Andy Grove was tapped as 1997’s person of the year. Intel shares were hammered a few years later, when the dot-com bubble burst.

Posted in Weekly Summary | No Comments »