Week of Sept 12 ’25 Weekly Recap & The Week Ahead

“There is a time to go long, a time to go short and a time to go fishing.” – Jesse Livermore

1. US Payrolls Marked Down a Record 911,000 in Preliminary Estimate— Annual revisions to nonfarm payrolls data for the year prior to March 2025 showed a drop of 911,000 from the initial estimates, according to a preliminary report from the Bureau of Labor Statistics. The total revision was on the high end of Wall Street expectations, which ranged from a low around 600,000 to as many as a million. The numbers, which are adjusted from data in the quarterly census and reflect updated information on business openings and closings, add to evidence that the employment picture in the U.S. is weakening. Most of the time span for the report came before President Donald Trump took office, indicating the jobs picture was deteriorating before he began levying tariffs against U.S. trading partners. The largest markdowns came in leisure and hospitality (-176,000), professional and business services (-158,000) and retail trade (-126,200). Most sectors saw downward revisions, though transportation and warehousing and utilities had small gains. Almost all the revisions were confined to the private sector; government jobs were adjusted down by 31,000.

2. US Producer Prices Unexpectedly Drop, First Decline Since April — The producer price index decreased 0.1% from a month earlier and July’s figure was revised down, according to a Bureau of Labor Statistics report out Wednesday. From the year before, the PPI rose 2.6%. Goods prices excluding food and energy rose 0.3%. Services costs fell 0.2%. Within services, margins at wholesalers and retailers fell 1.7%, matching the biggest drop in data going back to 2009 and reversing an outsize increase in July. Margins have been volatile from month to month so far this year, underscoring uncertainty around the impact of trade policy on prices and demand.

3. US Core CPI Rises as Expected, Keeping Fed on Track for Rate Cut — The core consumer price index, excluding the often volatile food and energy categories, increased 0.3% from July, according to Bureau of Labor Statistics data out Thursday. When incorporating those components, the overall CPI rose 0.4%, the most since the start of the year. Goods prices, excluding food and energy, accelerated 0.3%, matching the biggest climb since May 2023. That reflected increases in new and used cars, apparel and appliances, which some economists pointed out as possible impacts of tariffs. But analysts were generally divided as to how much of a role the duties played in the report, with others more focused on surges in travel-related services like airfares and hotel stays. Several household expenses also picked up, including groceries, gasoline, electricity and car repairs.

Taken together, the report suggests inflation continues to linger. President Donald Trump’s global tariffs are impacting prices of some goods, while ongoing increases in services costs may present a more persistent pressure to overall inflation.

4. Jobless Claims Rose Sharply Last Week — In the week through Sept. 6, jobless claims filings rose to 263,000, up from 236,000 a week earlier. Economists polled by The Wall Street Journal were forecasting 235,000 claims. Continuing claims, an indicator of the size of the total unemployed population, came in at 1.94 million in the week through Aug. 30, level from a week earlier. The continuing-claims data lag the initial-claims data by a week.The pace of job creation has fallen off significantly over the summer, prolonging workers’ job searches. But so far this year, there hasn’t been much sign of a big increase in layoffs.

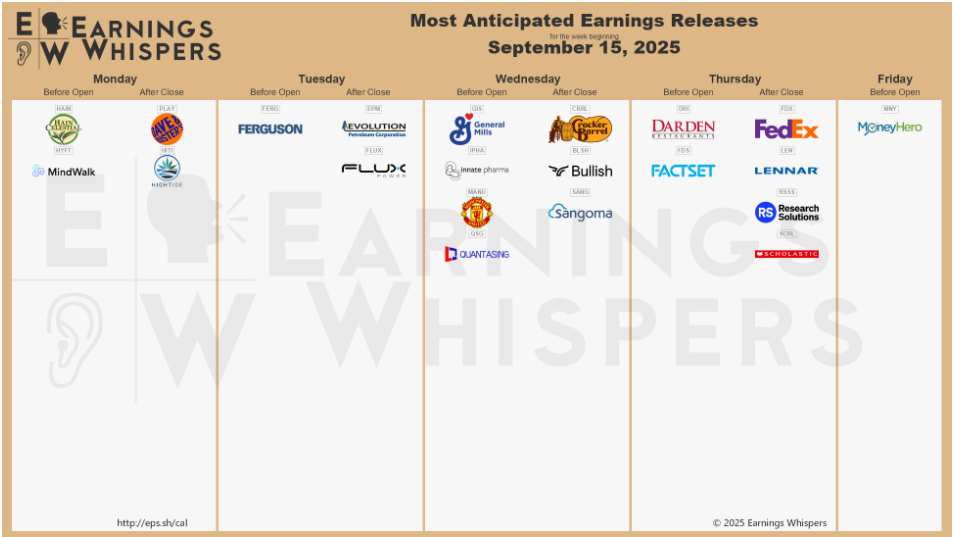

The week ahead — Economic data from Econoday.com: