Week of Dec 13, 2024 Weekly Recap & The Week Ahead

“Knowledge born from actual experience is the answer to why one profits; lack of it is the reason one loses” — Gerald M. Loeb

1. Inflation Ticked Up to 2.7% in November — The consumer-price index rose 2.7% from a year earlier, the Labor Department said Wednesday, after climbing 2.6% in October. Core prices, which exclude volatile food and energy items, rising 3.3% over the previous 12 months. The CPI index rose 0.3% from the prior month, the strongest month-over-month increase since April. The increase was driven by persistent inflationary pressures in the cost of food, vehicles and medical care. The pace of housing-cost increases cooled slightly from the prior month, which economists said was a welcome development. But they voiced concerns about persistent inflation in the services sector, which makes up the lion’s share of U.S. economic activity. Core goods inflation also picked up from the prior month, led by a jump in vehicle prices.

2. OPEC Makes Deepest Cut Yet to 2024 World Oil Demand Forecast — The Organization of Petroleum Exporting Countries chopped projections for consumption growth in 2024 by 210,000 barrels a day to 1.6 million barrels a day, according to its monthly report. The cartel has slashed projections by 27% since July as it belatedly recognizes the deteriorating market picture. Last week, the OPEC+ alliance led by Saudi Arabia and Russia agreed for a third time to delay plans to restart halted crude production, while also slowing the pace of increases once they do begin next year. The first in a scheduled series of hikes was postponed to April from January. Oil prices have declined 17% since early July as China falters and supply from OPEC’s rivals in the Americas booms. Brent futures are trading near $73 a barrel, too low for the Saudis and many others in the coalition to cover government spending.

3. Wholesale prices rose 0.4% in November, more than expected — The producer price index, or PPI, which measures what producers get for their products at the final-demand stage, increased 0.4% for the month, higher than the Dow Jones consensus estimate for 0.2%. On an annual basis, PPI rose 3%, the biggest advance since February 2023. However, excluding food and energy, core PPI increased 0.2%, meeting the forecast. Also, subtracting trade services left the PPI increase at just 0.1%. The year-over-year increase of 3.5% also was the most since February 2023. Final-demand goods prices leaped 0.7% on the month, the biggest move since February of this year. Some 80% of the move came from a 3.1% surge in food prices, according to the BLS.

4. ‘Wanted’ Signs Targeting Wall Street and Healthcare Executives Pop Up in New York City — “Wanted” posters threatening healthcare and Wall Street executives have gone up around New York City, the latest escalation of vitriol since last week’s assassination of a UnitedHealth executive.

The posters seen around lower Manhattan this week showed the names and faces of Wall Street and healthcare executives. The signs encouraged violence against them. “Health care CEOs should not feel safe,” the posters said. One displayed Brian Thompson, the UnitedHealthcare chief who was killed, with a red X over his face. The posters dragged conversations about corporate violence from the internet into the real world. Some people online have said Thompson’s death outside a Midtown hotel was justified because he ran a company that denied patients lifesaving care. The same pockets are holding up Mangione as a quasi-folk hero who exposed long-simmering anger at the U.S. healthcare system.

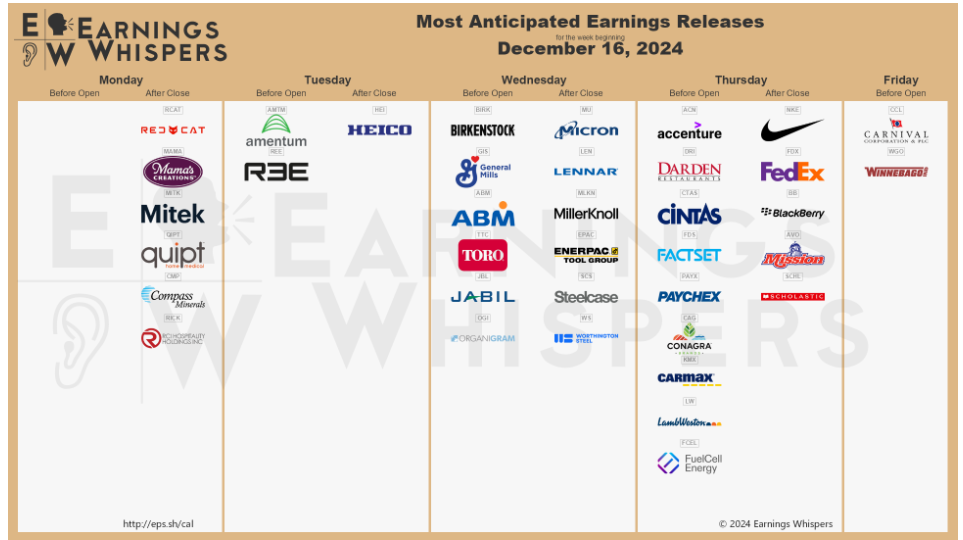

The week ahead — Economic data from Econoday.com:

This entry was posted

on Monday, December 16th, 2024 at 5:10 pm and is filed under Weekly Summary.

You can follow any responses to this entry through the RSS 2.0 feed.

You can leave a response, or trackback from your own site.

This entry was posted

on Monday, December 16th, 2024 at 5:10 pm and is filed under Weekly Summary.

You can follow any responses to this entry through the RSS 2.0 feed.

You can leave a response, or trackback from your own site.