Week of May 3, 2025 Weekly Recap & The Week Ahead

Wednesday, May 7th, 2025“It takes 20 years to build a reputation and five minutes to ruin it.” — Buffetts

1. U.S. Economy Contracts at 0.3% Rate in First Quarter — the Commerce Department said U.S. gross domestic product—the value of all goods and services produced across the economy—fell at a seasonally and inflation adjusted 0.3% annual rate in the first quarter. That was the steepest decline since the first quarter of 2022. Net exports, the difference between imports and exports, were a large drag on growth in the first quarter, stripping 4.83 percentage points from headline GDP. Imports increased at a 41.3% pace in the first quarter as businesses tried to get ahead of tariffs that began to come into effect during the first three months of the year and were dramatically increased in the current, second quarter. The GDP report is the first major economic scorecard for the January-to-March quarter, a period in which the White House changed hands from President Joe Biden to President Trump. January—most of which was before Trump took office—was hit by wildfires in Los Angeles and disruptive winter storms in many parts of the country.

2. US Manufacturing Activity Shrinks by the Most Since November — The Institute for Supply Management’s factory gauge eased 0.3 point to 48.7, data out Thursday showed. The group’s production index stumbled more than 4 points to 44. Readings below 50 indicate contraction. Prices paid for inputs, however, accelerated slightly. The figures illustrate an industrial sector struggling for traction as US tariffs and general uncertainty surrounding trade policy interrupt expansion plans. Orders shrank for a third month and backlogs retreated at a faster pace, consistent with subdued demand.

3. US Consumer Spending Jumps While Key Inflation Gauge Slows Down — Inflation-adjusted consumer spending climbed 0.7% last month, according to Bureau of Economic Analysis data out Wednesday. That was the most since the start of 2023 and suggested households spent aggressively to get ahead of new tariffs.

Meantime, the Federal Reserve’s preferred inflation gauge — the personal consumption expenditures price index — stagnated from a month earlier for the first time in nearly a year. Excluding food and energy, the so-called core PCE was also unchanged, the tamest in almost five years. The data round out a quarter in which the US economy contracted for the first time since 2022 on a monumental pre-tariffs import surge and more moderate consumer spending. The report earlier Wednesday also showed core PCE inflation accelerated to a 3.5% pace in the first quarter — the most in a year.

4. U.S. payroll growth totals 177,000 in April, defying expectations — Nonfarm payrolls increased a seasonally adjusted 177,000 for the month, slightly below the downwardly revised 185,000 in March but above the Dow Jones estimate for 133,000, the Bureau of Labor Statistics reported Friday. The unemployment rate held at 4.2%, as expected, indicating that the labor market is holding relatively stable. The survey of households, which is used to calculate the jobless rate, showed an even stronger gain, with an increase of 436,000 in those who reported holding jobs on the month.

A broader unemployment gauge that includes discouraged workers and those holding part-time jobs for economic reasons, or the underemployed, edged lower to 7.8%. The labor force participation rate ticked higher to 62.6%. The strong report led traders to push out expectations for an interest rate cut until July, according to the CME Group’s FedWatch gauge of futures pricing.

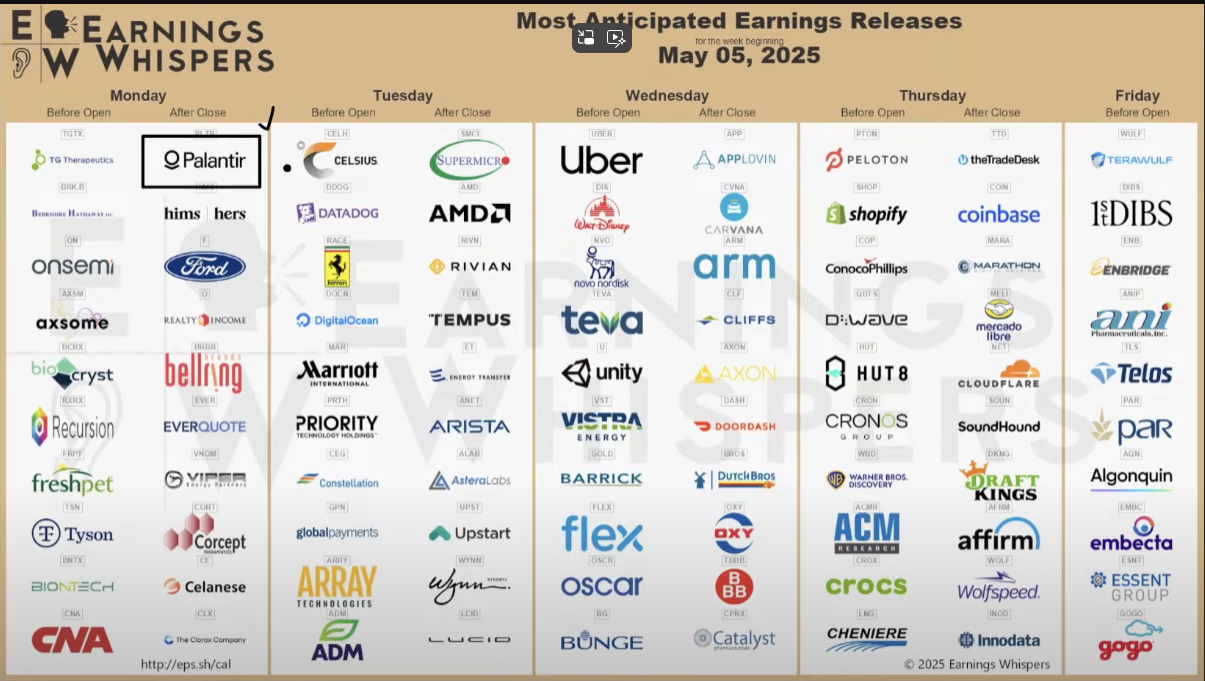

The week ahead — Economic data from Econoday.com: