Week of May 17, 2025 Weekly Recap & The Week Ahead

Thursday, May 22nd, 2025“Do more of What Work and Do Less of What Doesn’t” — unknown

1. U.S. and China agree to slash tariffs for 90 days in major trade breakthrough — The trade agreement means that “reciprocal” tariffs between both countries will be cut from 125% to 10%. The U.S.′ 20% duties on Chinese imports relating to fentanyl will remain in place, meaning total tariffs on China stand at 30%. The breakthrough comes after U.S. and China trade representatives held high-stakes talks in Switzerland over the weekend. The pause will begin Wednesday. Both China and the U.S. said they will continue discussions on economic and trade policy.

2. Monthly Inflation Ticked Up in Early Hints of Tariff Effects — The consumer-price index rose a seasonally adjusted 0.2% in April, the Labor Department said Tuesday. That matched the forecasts of economists polled by The Wall Street Journal. However, it was a turnaround from March, when month-over-month prices fell 0.1%. Year-over-year inflation cooled to a 2.3% increase in April, below the 2.4% that economists had expected and below March’s annual rate. A big decline in gasoline prices versus a year earlier helped pull that rate lower. Prices excluding food and energy categories—the so-called core measure that economists watch in an effort to better capture inflation’s underlying trend—rose 2.8%. That matched forecasts by economists.

3. US Producer Prices Fell Unexpectedly in April as Margins Shrank — The 0.5% decrease in the producer price index followed no change in March, Bureau of Labor Statistics data showed Thursday. The median forecast in a Bloomberg survey of economists called for a 0.2% gain. Excluding food and energy, the PPI declined 0.4% — the most since 2015. Stripping out food, energy and trade, a less-volatile measure favored by many economists, prices fell 0.1%, the first decline in five years. Compared with a year ago, the gauge rose 2.9%. The figures suggest American manufacturers and service providers are so far refraining from passing along higher US duties on imports. The impact on consumers has also been modest even as producers are feeling the pinch from aggressive levies on imported materials and other inputs.

4. US Retail Sales Barely Rise, Suggesting Some Spending Pullback — Growth in US retail sales decelerated notably in April, reflecting consumers pulled back spending on cars, sporting goods and other categories of imported goods amid concerns about rising prices from tariffs.

The value of retail purchases, not adjusted for inflation, increased 0.1%, Commerce Department data showed Thursday. That followed a a revised 1.7% gain in March, which was the largest in two years. Seven of the report’s 13 categories posted decreases, also restrained by apparel — another good which is largely imported — as well as gasoline. Car sales declined slightly after a buying spree in the previous month. Spending at restaurants and bars, the only service-sector category in the retail report, rose firmly for a second month.

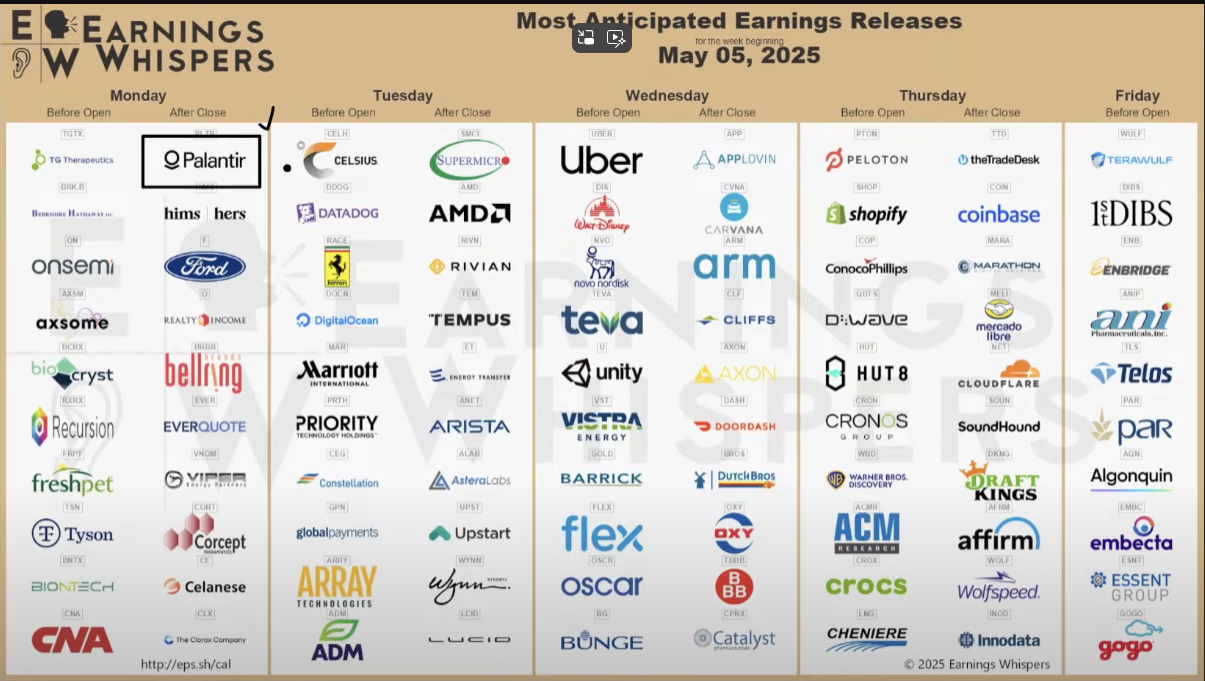

The week ahead — Economic data from Econoday.com: