Week of Sept 20, 2024 Weekly Recap & The Week Ahead

Wednesday, September 25th, 20241. US Retail Sales Post Surprise Gain, Helped by Online Stores — The value of retail purchases, unadjusted for inflation, increased 0.1% after a revised 1.1% gain in July, Commerce Department data showed Tuesday. Excluding autos and gasoline stations, sales advanced for fourth month. Five of the report’s 13 categories posted increases, while others such as electronics and appliances, clothing and furniture fell. E-commerce merchants posted a solid 1.4% gain. Receipts at gasoline service stations decreased, reflecting cheaper prices at the pump.

The retail sales report showed so-called control-group sales — which are used to calculate gross domestic product — rose 0.3% in August. The measure excludes food services, auto dealers, building materials stores and gasoline stations.

2. Fed Cuts Rates by Half Point in Decisive Bid to Defend Economy — The Federal Reserve lowered its benchmark interest rate by a half percentage point Wednesday, an aggressive start to a policy shift aimed at bolstering the US labor market. Projections released following their two-day meeting showed a narrow majority, 10 of 19 officials, favored lowering rates by at least an additional half-point over their two remaining 2024 meetings. Seven policymakers supported another quarter-point rate reduction this year, while two opposed any further moves. The Federal Open Market Committee voted 11 to 1 to lower the federal funds rate to a range of 4.75% to 5%, after holding it for more than a year at its highest level in two decades. It was the Fed’s first rate cut in more than four years.

3. Jobless Claims: Weekly jobless claims remained stable, suggesting a strong labor market.

4. Consumer Spending: Retail sales saw moderate growth, reflecting healthy consumer spending, though some sectors raised concerns about potential slowdowns.

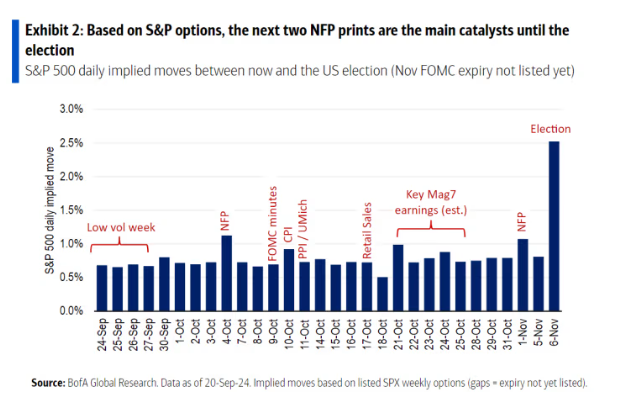

5. The Most Volatile Days for Stocks Before the Election, According to the Options Market — according to a team of strategists at Bank of America, who plotted what options traders are expecting each day before expiry. Traders anticipate swings of more than 1% in either direction on Oct. 4 and Nov. 1, when the September and October jobs reports are due to be released. Two other economic reports also have notable market-moving potential: the September CPI report, due Oct. 10, and the September retail sales report, on Oct. 17.

Options are also bracing for a roller-coaster ride during the week that starts on Oct. 21, one of the busiest of the coming third-quarter earnings reporting season. The week will feature results from Alphabet Inc., Microsoft, Meta and Amazon.

The week ahead — Economic data from Econoday.com: